It definitely seems like BS to me. At 3% it's 258% over 32 years (1.03^32). Most people are barely getting 1% annual raises which means income increases by 138% over the same period. From 1984 to 2016 housing prices in the Greater Vancouver area have gone up 800% [1].

Assuming I got the math right, it doesn't take much to see current young people are getting screwed. In the last 4 decades wages have barely increased, but major assets like cars and houses are 8-10x what they used to be.

Add in the cost of schooling for 2 people, which in my mind roughly translates to the cost of 2 brand new cars for my parent's generation, and it's easy to see why young people can't afford anything.

Then consider that "household" income is coming from 2 income earners now vs 1 income earner 40 years ago and you really start to get a picture of how tough it is.

How is anyone supposed to start a family when they can't afford to start thinking about buying a house until they're 35. Frugal people from my parent's generation could have their house paid off by the time they were 35.

You're perspective is skewed by living in one of the craziest housing markets in the world. Here in exurban Maryland (not to mention say Kansas City or Iowa) young people are buying homes and having kids.

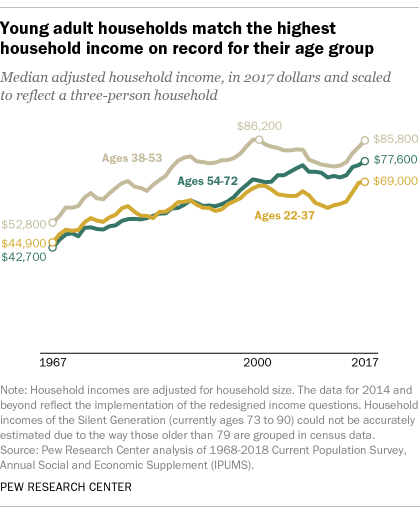

Also, two-earner households were already the majority since the late 1960s: https://files.taxfoundation.org/legacy/docs/22.jpg. The percentage of households where only the husband works dropped a bit from 1980-1990, but has been basically unchanged in the last 3 decades.

The thing you're overlooking is that the median young person lives in Kansas City (or whatever the equivalent is for Canada), not Vancouver. Those young people living in Vancouver are getting screwed for sure. They should vote out the liberal governments causing housing prices to skyrocket through overregulation, causing credential inflation by throwing money at universities, etc. Or they can move to Kansas!

>>> They pay less on a monthly mortgage payment than their parents did

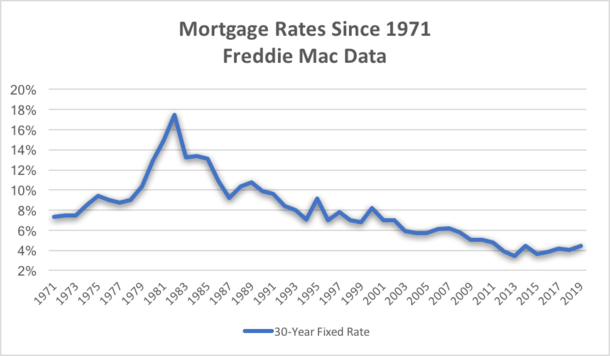

The reference you gave for "They pay less on a monthly mortgage payment" is itself adjusted for inflation as noted on the chart. So using the questionable inflation figure itself to refute inflation isn't persuasive.

Intuitively also, I'm not sure I buy the argument that the median young person lives in Kansas City. I grew up with dozens of family members who actually did live in middle america (most of them as engineers at car plants.) Many of those jobs are not as cushy as they once were. Some are gone. From my own experience as an engineer, the weighted centroids of the job market are in SF or NY or DC, not in Ohio.

Of course, that is an engineering viewpoint, what about overall across professions? I dont quite understand this and i'd love to be educated. From everything I read, the traditional jobs in middle america have left and these towns struggle. My own experience is only anecdotal (e.g., upstate NY, western pennsylvania)

> The reference you gave for "They pay less on a monthly mortgage payment" is itself adjusted for inflation as noted on the chart. So using the questionable inflation figure itself to refute inflation isn't persuasive.

Yes, it's adjusted for inflation. But if housing costs were growing faster than inflation, the monthly mortgage payment adjusted for inflation would still be going up.

> My own experience is only anecdotal (e.g., upstate NY, western pennsylvania)

Head down to Kansas City, or east Texas, or pretty much anywhere in the sunbelt. These places are booming. They're full of young people, families, and tons of kids.

> Most people are barely getting 1% annual raises which means income increases by 138% over the same period.

Where is that 1% coming from? It seems to me US salaries growth pretty much followed 3/5% average for the last 50 years, with some obvious drawdowns during crises.

> In the last 4 decades wages have barely increased, but major assets like cars and houses are 8-10x what they used to be.

That doesn't make any sense. The price of a good should roughly follow an optimum of supply and demand. There is of course a spectrum in which it can oscillate, but your "barely increased" versus "8-10x" comparison is ridiculous.

Things are evolving inside a pretty much closed system. Of course that's not exactly true, especially with capital movements, and mondialisation, but the ballpark should be there. You cannot take conclusions if you don't study the full picture.

Take housing prices for instance. The main driver for real estate is not some conspiracy of evil super wealthy people. It's just the interest rates. If interest rates lower, then borrowing money is cheaper, people get bigger mortgages, which in turn inflates real estate prices.

> From 1984 to 2016 housing prices in the Greater Vancouver area have gone up 800% [1].

Real estate cannot be studied in geographical isolation. There are way too much factors that can cause local inflation. In the case of Vancouver's real estate, it is notoriously the flow target of a lot of Asian capital. I don't think that should be taken as an example.

That is almost exactly an increase of 8X, compared to roughly 1.5X for personal income. Do you think an increase of 1.5X over forty years or so counts as "barely increased"?

Of course household income is higher because most households have two wage earners instead of one. But that's still around 3X to around 8X.

And the standard deviation for property prices has increased hugely.

This has nothing to do with supply and demand and everything to do with the difference between an unproductive rent seeking economy which sweats static assets - including the workforce - and a productive creative economy driven by innovation and invention.

For all the rhetoric, the current economy has a lot more of the former than the latter. And this is only good for a small number of incredibly rich individuals - at the expense (literally) of almost everyone else.

I think these graphs mistakenly compare inflation adjusted wages to unadjusted house price. It also fails to account for increases in house size.

Inflation adjusted cost per square foot is $126 in 1978 and $146 in 2020, about a 16% increase. Inflation adjusted wages over the same years went from 24.5K in '78 to 36K in '19, for about a 46% increase.

According to these stats, housing is actually more affordable for the same home size.

I wonder to what extent homes have increased in size to compensate for the higher price of the land they are built on.

In my neighbourhood over the last ten years small-ish 1-floor homes built in the 70s and 80s have been consistently replaced with 3-story McMansion atrocities.

You can't buy a smaller, cheaper, house because they are not being built, and I suspect the reason I'd that their price per square foot would be sky high due to the cost of the land.

What I am saying is that the price of a good (say, a car) is not decided in a vacuum. It is merely an indirect side effect of the supply and demand optimum.

What that means is that if the price of cars increases, it is a consequence of either consumers being willing/able to pay more for a car (demand driven) or cars being more expensive to build (supply driven). As I mentioned, this is not an absolute truth, since the term structure of the supply demand _could_ change due to external factors. I still mention that in the case of these goods, this is very unlikely.

For housing, the main factors are 1) what the investment will yield (rent expectation) 2) what the investment costs (interest rates).

If any of these factors (rent, IR) changes, it will impact the price.

> Here's a graph of median personal income:

> And here's a graph of median house prices:

You are comparing CPI adjusted versus point in time dollars here...

Is the source taking the average or median for wage growth? I'd expect that the average has gone up because of the insane growth in executive pay. But I'd be interested in seeing the change in the median, which I'm sure is much less than the average.

It is not that simple. I crashed out of my first career (with student loans in a STEM field), then learned to program at age 27. I’ve been tremendously lucky and successful in the decade since then, lived in a tiny place in SF for years (with a growing family) while working big tech, and I’m only just now at a point I can get my family into a house.

I’m one of the lucky ones. Learning the skills is not enough, you have to get a very good job and work your ass off for a decade for it to amount to enough to comfortably afford the housing, education, and healthcare for a family.

A generation ago getting that kind of quality job was much easier and just having the job put you in the family-supporting income range.

No. The original scalable solution to low growth is government R&D seed funding spreading out into innovation in the consumer economy.

You're not going to get much growth if all you do is educate people. You also need to give them something to do, and that requires a national investment strategy.

This is exactly the difference between the insanely productive post-war economy, which developed and then commoditised electronics and computing, and the modern lazy bullshit job economy which is built on financialised gambling-at-scale and ad tech rather than game-changing creative invention.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Assuming I got the math right, it doesn't take much to see current young people are getting screwed. In the last 4 decades wages have barely increased, but major assets like cars and houses are 8-10x what they used to be.

Add in the cost of schooling for 2 people, which in my mind roughly translates to the cost of 2 brand new cars for my parent's generation, and it's easy to see why young people can't afford anything.

Then consider that "household" income is coming from 2 income earners now vs 1 income earner 40 years ago and you really start to get a picture of how tough it is.

How is anyone supposed to start a family when they can't afford to start thinking about buying a house until they're 35. Frugal people from my parent's generation could have their house paid off by the time they were 35.

1. https://www.huffingtonpost.ca/ypnexthome/canadas-housing-per...